{kind=link}

The keys to home ownership in Canada are now harder to reach than ever. Meanwhile, the keys to the Canadian Mortgage Market have just been handed to the Big 6 Canadian Banks. Continue reading →

Call Us: 416 766 9000 info@morcandirect.com

The keys to home ownership in Canada are now harder to reach than ever. Meanwhile, the keys to the Canadian Mortgage Market have just been handed to the Big 6 Canadian Banks. Continue reading →

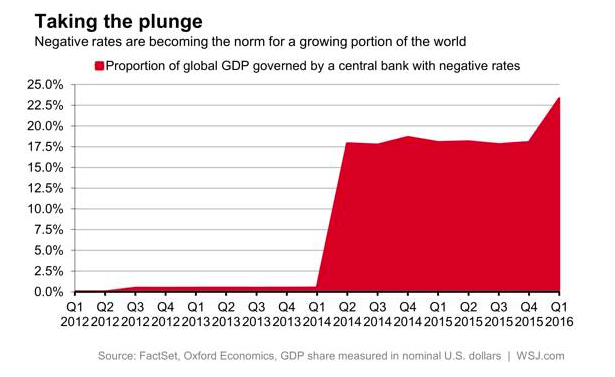

A major trend in the world economy is for Central Banks to favour reducing interest rates to negative levels in an attempt to spurn financial growth. Currently, economies that account for about 25% of global economic output are governed by negative rates and this is trending higher. It’s OK to be excited about lower mortgage rates, but you should also be concerned about our increased dependency at the macro level to rely on such low rates.

Economists predict 50% chance Bank of Canada will Drop Rates in 2016.

If a Fixed Rate Mortgage is insurance against a growing economy, do you really need to buy it right now?

The market believes there is a 50% chance the Bank of Canada will decrease the overnight rate this week. This will send our weak Canadian Dollar even lower, and might not be in Canadians’ best interest.

Did you catch CBC’s The National discussing increasing Canadian mortgage debt with MorCan Direct last night?

Canadian real estate owners have found themselves in an enviable position over the past 10 to 15 years. Our property values continue to increase and, with few exceptions, the cost to borrow continues to decrease. In 2015 alone, we saw the Bank of Canada reduce interest rates twice. Continue reading →

Dilip and Geeta purchased their first home in 2012. They went to their Big 5 bank who had a 5 year fixed rate of 4.79%, but offered them a ‘discounted’ rate in the mid 3’s. This summer they finally got fed up hearing how their friends were all paying closer to 2.0% on 5 year variables. They went to their bank to ask about switching into a lower rate variable. Continue reading →

Now’s the time to act. The ultra low variable rates we’ve enjoyed for most of the year are going into hibernation. Last week a few leading lenders tightened up their guidelines for qualifying borrowers. Over the weekend a few more lessened the discount off the prime rate they’ve been offering, by up to 15 basis points. And tonight, alas, everyone else seems to be following suit.

Danny was a self-employed contractor who owned both his principal residence and a rental property. He had been using as many deductions as possible at tax time, so his taxable income was quite low in comparison to the amount of business he had performed. His income was also quite varied from year to year. Because of the deductions and variations, his bank would only offer him a new mortgage with a hefty premium attached. Continue reading →

Government of Canada Bond Yields immediately dropped by 5% in the wake of the announcement. The Loonie on the other hand rose slightly, while a further dip was likely had there been a rate hike. Oil wasn’t noticeably affected by the announcement, but overall the markets certainly approved.

“Monetary Policy will remain significantly accommodative for quite some time.”

US GDP expanded at 2.25% in the first half of 2015 which was stronger than the Fed expected. However, Inflation is running below the Feds objective.”

There are many factors at play that lead to the Fed’s decision to keep rates where they are and maintain an accommodative monetary policy.

Although most Fed insiders continue to believe that rates will increase in 2015, some participants now believe that a rate hike should be put off until 2016. But regardless of when the hike occurs, and by how much, the Fed was very clear that their policies would remain highly accommodative for some time. If and when rates do begin to increase, they will likely increase very slowly and be accompanied by continued monetary stimulus.

George lost his job a month before Margot had their first baby. Turning to their bank, they were offered a lot of unsecured debt at high interest rates which they accepted in a panic. Over the next few months, with increasing living expenses for the baby, their credit began a downward spiral. When George finally returned to work, their credit was so low the same bank that had previously been so generous now wouldn’t even renew their mortgage. Continue reading →

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}