Newton’s third law states that for every action there is an equal and opposite reaction. Newton can probably help us figure out how many more interest rates hikes we have in store for us. His law may also be useful in countering the claim the interest rates will continue to increase in the next two years without pause.

First off, let’s take stock of where we are right now. The Bank of Canada has set their benchmark rate to 1%. This means that the prime rate is now 3.2%. Since variable-rate mortgages are priced off of Prime many Canadians will soon be feeling the pinch of higher mortgage rates.

So. What should you do? Is it time to take a fixed rate, or should you stay variable?

Staying variable has never been for the faint of heart, and lately you seem to need a cardiologist on speed dial to opt out of taking a fixed rate. In addition to changing monetary policy the mortgage rate environment is also rather complex right now. Whether you are in the fixed or variable rate mortgage camp, all rates are now affected by new factors like whether a borrower is buying or selling, how much equity they have, and the dollar amount of their loan.Like this article? Click here to receive our newsletter every time!

Before we go any further, I can tell you that MorCan Direct is still offering a 5 year fixed rate of 2.85%. According to market consensus, Canadians could be in store for 2 more rate hikes between now and May 2018 and considering that our Variable Rate Mortgages run at about Prime – 0.80%, if we can qualify you for the 5 year fixed rate, now might not be bad time to lock in.

In today’s newsletter we will look at why you may want to take a fixed rate versus a variable rate and what Newton’s third law means to each decision. Then we will discuss why this sudden interest rate hike happened and what it might mean. Sound like fun?Like this article? Click here to receive our newsletter every time!

Fixed Rate Argument:

- The Rate: At 2.85%*OAC on a 5 year fixed rate you are buying a discount to prime for the next 5 years. This is a very safe place to wait out the next 12 months of uncertainty.

- The Market: Since May 2017 Bond yields have increased by 0.70%! You can check the graph here, but this means fixed rates certainly have additional pressure to move higher.

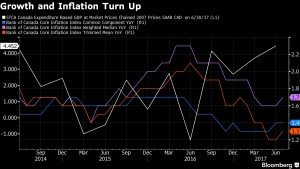

- The Economy: Canadian growth numbers have looked strong for the past few months (April, May and June), with GDP (the white line in the graph below) increasing for 8 consecutive months. Although inflation still isn’t where economists would like to see it consumer spending, employment, and GDP growth certainly do paint a rosy picture of the Canadian economy.

- Newton’s Third Law: Canada and the world have been extremely accommodative with their monetary policy for almost 10 years. The reaction may very well be a strengthening economy that is not as heavily reliant on real estate and borrowing as economists had predicted. Based on the very recent economic data Canada appears to be heading into a period of economic expansion.

Like this article? Click here to receive our newsletter every time!

With all of that information, why would anyone tell you to go variable? There is still another side to this argument.

Variable Rate Argument:

- The Rate: Variable rate mortgages are still very attractively priced, between 2.4%*OAC and 2.6%*OAC, depending again on the type of mortgage you are looking for. Additionally, the variable-rate mortgage is far more flexible when it comes to breaking, especially if you’re dealing with one of the big banks.

- The Market: Although bond yields have seen a tremendous uptick in the past few months, fixed-rate mortgages are still not priced as high as they usually are relative to those bond yields. Finally, longer-term bond yields aren’t showing us that the market really believes we are in a long-term rate-increasing environment yet.

- The Economy: A slowing real estate market isn’t reflected in the economic numbers yet. Make no mistake, our economy will be impacted by this increase in borrowing rates. Along with the much stronger dollar, and the drop in housing prices, policymakers must be careful with how hard they pump the brakes on the Canadian economy.

- Newton’s Third Law: The period of economic expansion that the Bank of Canada is referencing for its rate increases is the last 6 months. Although they were probably right in increasing the overnight rate by 0.50% from the ultra-low rates we have enjoyed, more caution will be needed with future rate increases. In the short term, we will probably see more strength from the Canadian consumer, more spending, and a stronger economy. My concern is that a weaker housing market and a stronger Canadian dollar will begin to weigh on the Canadian economy. The Bank of Canada has clearly proven that it will act based on data and not on market expectations. The next Bank of Canada meeting is on October 25th, 2017, and although it is unlikely they will increase rates again, more signs of strength in the Canadian economy might lead to another increase.

Why Did This Move Catch Everyone Off Guard?

One economist from BMO went so far as to call out the Bank of Canada for their lack of communication with the Canadians. To be sure, many economists felt that a little more communication would have been nice. The Bank of Canada feeling the pressure even responded to all the criticism in a statement, defending its actions. It wasn’t too long ago that all central banks behaved in this manner. No guidance was given, banks simply announced a decision when they saw fit based on the numbers, no press releases, no press conferences mandated before and after an announcement, no hand holding of the economists and the press.

There are three reasons why this announcement could have caught everyone off guard:

- Perhaps this is a nod towards the strength of the Canadian economy. While Central Bankers around the world are being very careful to not rattle markets by speaking slowly, and carefully, and clearly telegraphing their moves, the Bank of Canada simply made a decision based on the economic data that it saw.

- Maybe the Bank of Canada got caught off guard a little by the strength in the numbers for the first 6 months of the year.

- The Governor of our Bank of Canada prefers not to provide forward guidance to markets. In fact he even wrote a paper on it before he became the Governor of the Bank of Canada in 2014. His belief is that instead of telegraphing the movement of the central bank, the bank should simply disclose all of the factors that are impacting the Banks decision and allow the market to assess new information just as the central bank does.

If you are still not sure what your best move is, give us a call today for sound, unbiased mortgage advice. One of our non-commissioned sales reps would be more than happy to look at your individual situation and give you advice on how to move forward. Alternatively, if you have a friend or family member thinking about the same decision, please forward them this article and let them know that they can call us as well.

Thanks,

Marcus Tzaferis